While sales tax holidays have been politically popular for a long time, they’ve seen a boost with lawmakers in several states this year as a way to share unanticipated surpluses with taxpayers. Although state budgets may be in unusual places this year, sales tax holidays remain the same as they always have been—ineffective and inefficient.

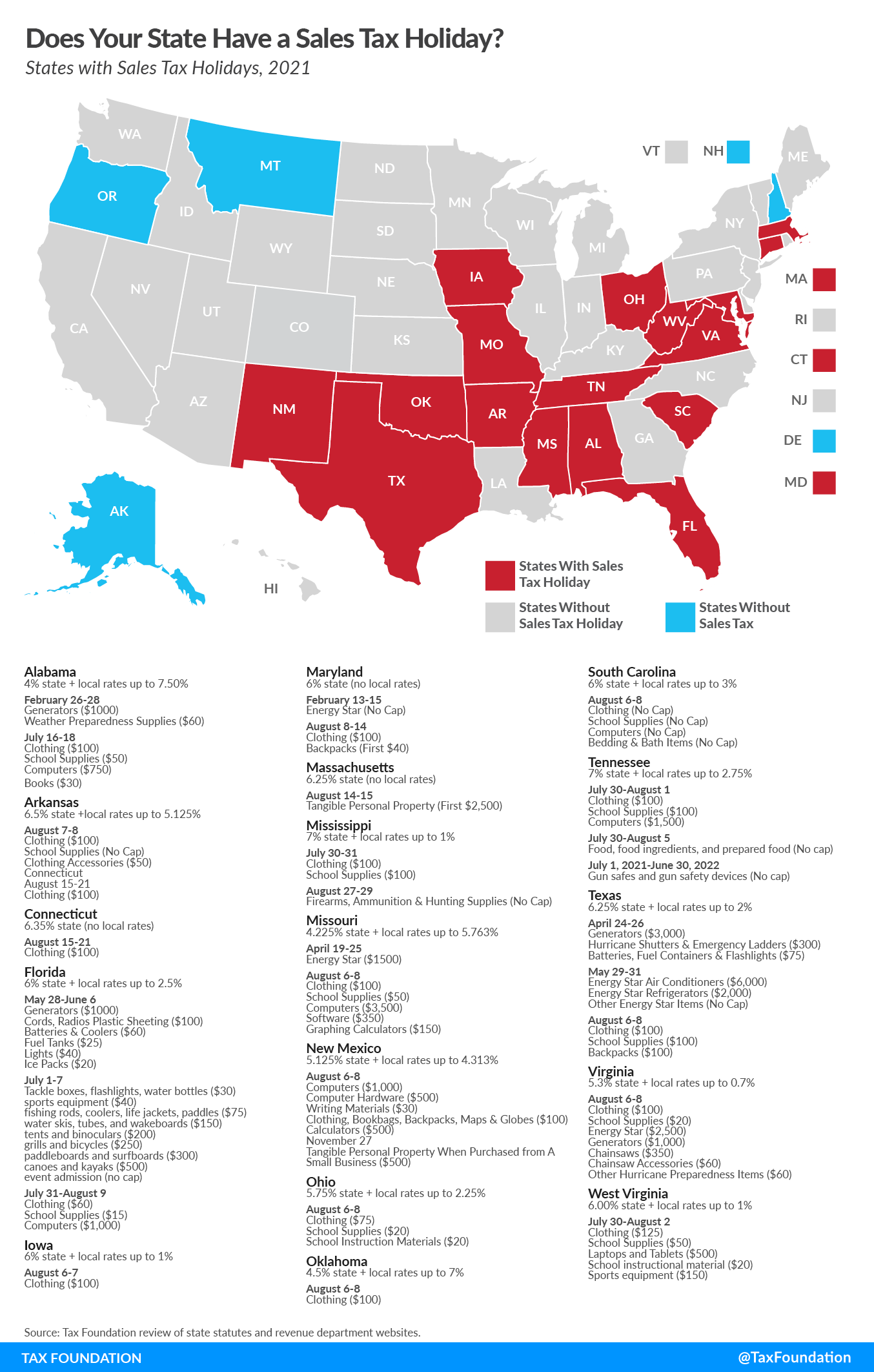

Seventeen states will hold a sales tax holiday in 2021, down from a peak of 19 in 2010, but above last year’s 16. This year, in addition to its regular tax-free weekend, Florida hosted a “Freedom Week” from July 1 to 7, exempting camping and outdoor hobby supplies from sales taxes. Tennessee increased its number of holidays by one, adding a year-long holiday for gun safety supplies beginning on July 1. Massachusetts Governor Charlie Baker (R) has pushed to extend the state’s holiday from a weekend to two months, but he does not appear likely to get this plan across the finish line.

Proponents argue that sales tax holidays promote economic growth. They posit that individuals will purchase more of the exempted goods than they would have in the absence of the holiday, and that they will also increase their consumption of nonexempt goods. However, the evidence (including a 2017 study by Federal Reserve researchers) shows that, instead of increasing purchases, consumers simply shift the timing of purchases they were already going to make. For most who shop during sales tax holidays, the exemptions simply provide a modest and unexpected benefit for doing something they would have done anyway.

The other prevalent argument is that sales tax holidays are a way of giving tax relief. This, too, is overstated. While sales taxes are somewhat regressive, this fact does not make sales tax holidays effective for providing relief to low-income individuals. To give small tax savings to those with lower incomes, holidays give large savings to higher-income groups as well.

Most sales tax holidays arbitrarily discriminate between products and create economic distortion. In the case of back-to-school holidays, backpacks may be exempt, for instance, but messenger bags may not be, influencing consumers to choose backpacks even if they would otherwise have chosen messenger bags. Likewise, a low-income or childless couple may have no need for school supplies, but they are presumably just as deserving of tax relief as those who purchase exempt products.

Such holidays discriminate across time. There is little economic justification for why a product purchased during one time period should be tax-exempt while the same product purchased in another time period should be taxable. Shifting purchases to a particular weekend is no more beneficial to the economy, all else being equal, than purchases in another time period. Additionally, some consumers may be unable to shop during the sales tax holiday because they are working, out of town, or between paychecks—situations that do not make anyone less deserving of tax relief.

Massachusetts’ sales tax holiday does not discriminate between products, as it applies to all tangible personal property, but still discriminates across time. Tennessee’s newest holiday has the opposite issue: it lessens time discrimination by lasting an entire year but favors only gun safety products.

In addition to not accomplishing their stated goals, sales tax holidays create complexities for tax code compliance, efficient labor allocation, and inventory management. However, free advertising for what is effectively a 4 to 7 percent discount leads many larger businesses to lobby for the holidays.

In the end, sales tax holidays are political gimmicks that distract from genuine, permanent tax relief. If a state must offer a “holiday” from its tax system, it is an implicit recognition that the tax system is uncompetitive. If policymakers want to save money for consumers, they should work to reduce the sales tax rate year-round.

For further discussion of sales tax holidays, see our report.

Does your state have a sales tax holiday?

{kind=link}

Note: The author would like to acknowledge the research assistance of Jeremiah Nguyen in compiling the data for this map.

Was this page helpful to you?

Thank You!

The Tax Foundation works hard to provide insightful tax policy analysis. Our work depends on support from members of the public like you. Would you consider contributing to our work?

Contribute to the Tax Foundation

Share This Article!

Let us know how we can better serve you!

We work hard to make our analysis as useful as possible. Would you consider telling us more about how we can do better?