Note: Each year we review and improve the methodology of the Index. For that reason, prior editions are not comparable to the results in this 2023 edition. All data and methodological notes are accessible in our GitHub repository. Below is an abbreviated version of the 2023 Index. To access the full report, click the download button above.

Introduction

The structure of a country’s taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

code is a determining factor of its economic performance. A well-structured tax code is easy for taxpayers to comply with and can promote economic development while raising sufficient revenue for a government’s priorities. In contrast, poorly structured tax systems can be costly, distort economic decision-making, and harm domestic economies.

Many countries have recognized this and have reformed their tax codes. Over the past few decades, marginal tax rateThe marginal tax rate is the amount of additional tax paid for every additional dollar earned as income. The average tax rate is the total tax paid divided by total income earned. A 10 percent marginal tax rate means that 10 cents of every next dollar earned would be taken as tax.

s on corporate and individual income have declined significantly across the Organisation for Economic Co-operation and Development (OECD). Now, most OECD nations raise a significant amount of revenue from broad-based taxes such as payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue.

es and value-added taxes (VAT).[1]

Not all recent changes in tax policy among OECD countries have improved the structure of tax systems; some have made a negative impact. Though some countries like the United States and France have reduced their corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.

rates by several percentage points, others, like Colombia, have increased them. Corporate tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.

improvements have occurred in Portugal, while the corporate tax base has been made less competitive in Belgium. The United States, the United Kingdom, and Chile are phasing out temporary improvements to their corporate tax bases.

The COVID-19 pandemic has led many countries to adopt temporary changes to their tax systems. Faced with revenue shortfalls from the downturn, countries will need to consider how to best structure their tax systems to foster both an economic recovery and raise revenue.

The variety of approaches to taxation among OECD countries creates a need to evaluate these systems relative to each other. For that purpose, we have developed the International Tax Competitiveness Index—a relative comparison of OECD countries’ tax systems with respect to competitiveness and neutrality.

The International Tax Competitiveness Index

The International Tax Competitiveness Index (ITCI) seeks to measure the extent to which a country’s tax system adheres to two important aspects of tax policy: competitiveness and neutrality.

A competitive tax code is one that keeps marginal tax rates low. In today’s globalized world, capital is highly mobile. Businesses can choose to invest in any number of countries throughout the world to find the highest rate of return. This means that businesses will look for countries with lower tax rates on investment to maximize their after-tax rate of return. If a country’s tax rate is too high, it will drive investment elsewhere, leading to slower economic growth. In addition, high marginal tax rates can impede domestic investment and lead to tax avoidance.

According to research from the OECD, corporate taxes are most harmful for economic growth, with personal income taxes and consumption taxA consumption tax is typically levied on the purchase of goods or services and is paid directly or indirectly by the consumer in the form of retail sales taxes, excise taxes, tariffs, value-added taxes (VAT), or an income tax where all savings is tax-deductible.

es being less harmful. Taxes on immovable property have the smallest impact on growth.[2]

Separately, a neutral tax code is simply one that seeks to raise the most revenue with the fewest economic distortions. This means that it doesn’t favor consumption over saving, as happens with investment taxes and wealth taxA wealth tax is imposed on an individual’s net wealth, or the market value of their total owned assets minus liabilities. A wealth tax can be narrowly or widely defined, and depending on the definition of wealth, the base for a wealth tax can vary.

es. It also means few or no targeted tax breaks for specific activities carried out by businesses or individuals.

As tax laws become more complex, they also become less neutral. If, in theory, the same taxes apply to all businesses and individuals, but the rules are such that large businesses or wealthy individuals can change their behavior to gain a tax advantage, this undermines the neutrality of a tax system.

A tax code that is competitive and neutral promotes sustainable economic growth and investment while raising sufficient revenue for government priorities.

There are many factors unrelated to taxes which affect a country’s economic performance. Nevertheless, taxes play an important role in the health of a country’s economy.

To measure whether a country’s tax system is neutral and competitive, the ITCI looks at more than 40 tax policy variables. These variables measure not only the level of tax rates, but also how taxes are structured. The Index looks at a country’s corporate taxes, individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S.

es, consumption taxes, property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services.

es, and the treatment of profits earned overseas. The ITCI gives a comprehensive overview of how developed countries’ tax codes compare, explains why certain tax codes stand out as good or bad models for reform, and provides important insight into how to think about tax policy.

Due to some data limitations, recent tax changes in some countries may not be reflected in this year’s version of the International Tax Competitiveness Index.

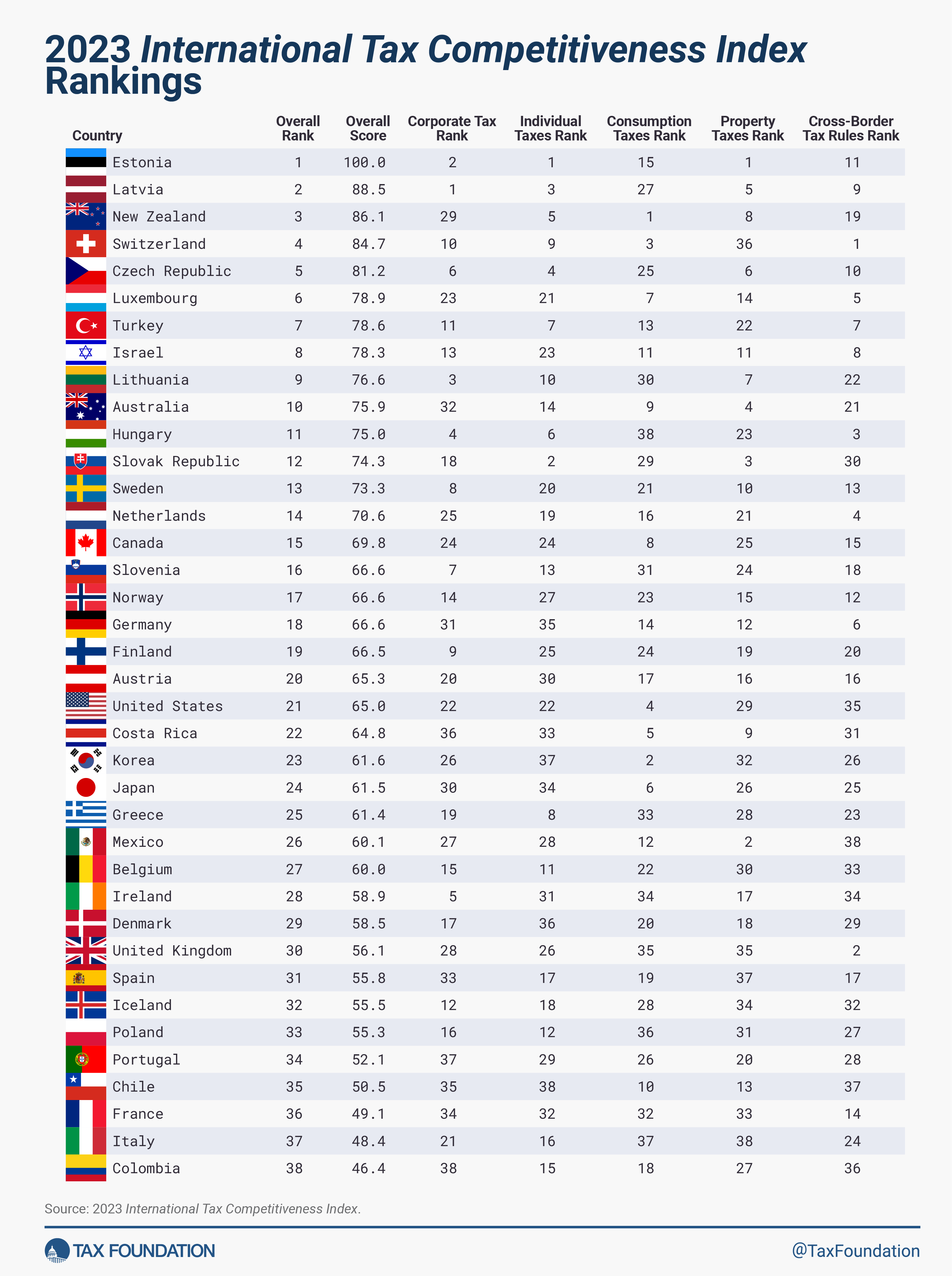

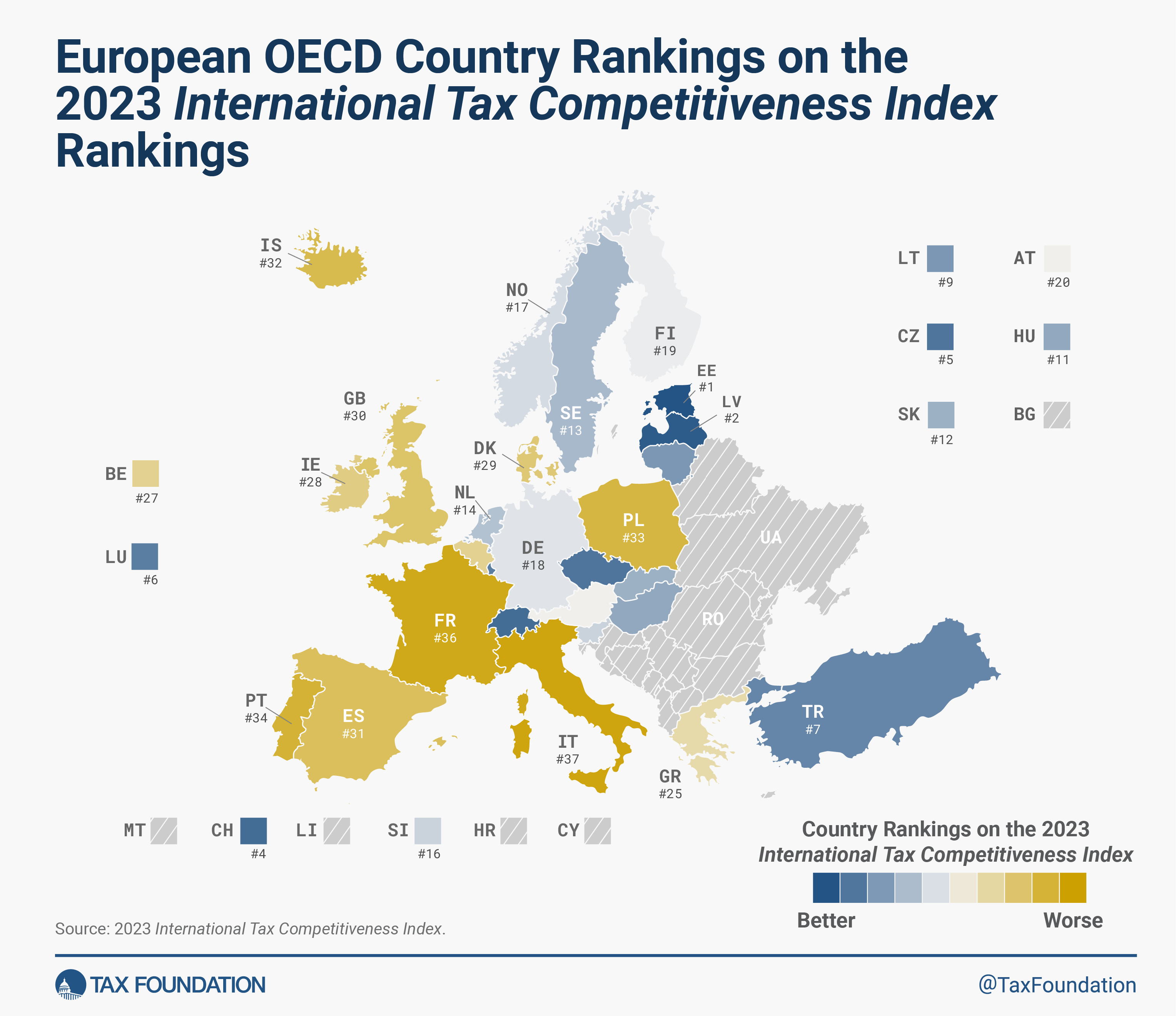

2023 Rankings

For the tenth year in a row, Estonia has the best tax code in the OECD. Its top score is driven by four positive features of its tax system. First, it has a 20 percent tax rate on corporate income that is only applied to distributed profits. Second, it has a flat 20 percent tax on individual income that does not apply to personal dividend income. Third, its property tax applies only to the value of land, rather than to the value of real property or capital. Finally, it has a territorial tax systemA territorial tax system for corporations, as opposed to a worldwide tax system, excludes profits multinational companies earn in foreign countries from their domestic tax base. As part of the 2017 Tax Cuts and Jobs Act (TCJA), the United States shifted from worldwide taxation towards territorial taxation.

that exempts 100 percent of foreign profits earned by domestic corporations from domestic taxation, with few restrictions.

While Estonia’s tax system is the most competitive in the OECD, the other top countries’ tax systems receive high scores due to excellence in one or more of the major tax categories. Latvia, which recently adopted the Estonian system for corporate taxation, also has a relatively efficient system for taxing labor income. New Zealand has a relatively flat, low-rate individual income tax that also largely exempts capital gains (with a combined top rate of 39 percent), a broad-based VAT, and levies no taxes on inheritance, property transfers, assets, or financial transactions. Switzerland has a relatively low corporate tax rate (19.7 percent), a low, broad-based consumption tax, and an individual income tax that partially exempts capital gains from taxation. Luxembourg has a broad-based consumption tax and a competitive international tax system.

Colombia has the least competitive tax system in the OECD. It has a net wealth tax, a financial transaction tax, and the highest corporate income tax rate of 35 percent. Colombia’s VAT covers less than 40 percent of final consumption, revealing both policy and enforcement gaps.

Italy has the second-least competitive tax system in the OECD. It has multiple distortionary property taxes with separate levies on real estate transfers, estates, and financial transactions, as well as a wealth tax on selected assets. Italy’s relatively high VAT rate of 22 percent applies to the fifth-narrowest consumption tax base in the OECD.

Countries that rank poorly on the ITCI often levy relatively high marginal tax rates on corporate income or have multiple layers of tax rules that contribute to complexity. The five countries at the bottom of the rankings all have higher than average combined corporate tax rates. Ireland ranks poorly on the ITCI despite its low corporate tax rate. This is due to high personal income and dividend taxes and a relatively narrow VAT base. Four out of the five lowest-ranking countries have unusually high top income tax thresholds, at 13 to 21 times the average income.

Notable Changes from Last Year

Australia

Australia introduced a patent boxA patent box—also referred to as intellectual property (IP) regime—taxes business income earned from IP at a rate below the statutory corporate income tax rate, aiming to encourage local research and development. Many patent boxes around the world have undergone substantial reforms due to profit shifting concerns.

in 2022. Australia’s rank decreased from 6th to 10th.

Belgium

Belgium limited carryforwards of losses from 70 percent to 40 percent of the taxable amount exceeding EUR 1 million in 2023. It also strengthened its controlled foreign company (CFC) rules. Belgium’s rank decreased from 22nd to 27th.

Chile

Chile phased out temporary full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs.

for machinery, industrial buildings, and intangible assets in 2023. It also broadened its VAT base in 2022 by eliminating exemptions. Chile’s rank fell from 31st to 35th.

France

France has been reducing its corporate income tax rate over several years, a process which concluded in 2022. As part of this scheduled reduction, France dropped its combined corporate rate (including a surtaxA surtax is an additional tax levied on top of an already existing business or individual tax and can have a flat or progressive rate structure. Surtaxes are typically enacted to fund a specific program or initiative, whereas revenue from broader-based taxes, like the individual income tax, typically cover a multitude of programs and services.

) from 28.41 percent in 2021 to 25.83 percent in 2022. Its Index rank remained unchanged at 36th.

Portugal

Prior to 2023, companies could carry forward losses of up to 70 percent of taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. For both individuals and corporations, taxable income differs from—and is less than—gross income.

for up to 12 years. Portugal now allows unlimited carryforwards of up to 65 percent of taxable income. Portugal’s rank rose from 35th to 34th.

Turkey

Turkey reduced its corporate tax rate from 23 percent in 2022 to 20 percent in 2023. Turkey’s rank rose from 10th to 7th.

United Kingdom

The UK phased out its 130 percent super-deductionA super-deduction is a tax deduction that permits businesses to deduct more than 100 percent of their eligible expenses from their taxable income. As such, the super-deduction is effectively a subsidy for certain costs. This policy sometimes applies to capital costs or research and development (R&D) spending.

for plants and equipment into full expensing. It also increased the main corporate rate from 19 percent in 2022 to 25 percent in 2023, while keeping a 19 percent reduced rate for small and medium-sized companies. The UK’s ranking dropped from 27th to 30th.

United States

The U.S. phased out full expensing for plants and equipment. It also decreased its implicit research and development (R&D) subsidy rate from 6.75 percent to 2.75 percent because R&D costs can no longer be expensed. The R&D subsidy rate for the U.S. is the lowest value in the OECD. The U.S. rank remained at 21.

Methodological Changes

Each year, we review the Index’s data and methodology to improve how it measures both competitiveness and neutrality. This year, we have changed the way the Index treats corporate taxes and individual taxes.

We have applied each change to prior years to allow consistent comparison across years. Data for all years using the current methodology is accessible in the GitHub repository for the Index,[4] and a description of how the Index is calculated is provided in the Appendix of this report. Prior editions of the Index, however, are not comparable to the results in this 2023 edition due to these methodological changes.

Corporate Tax

The surtax rates on corporate income have been replaced by dummies indicating the existence of surtaxes on corporate income. The surtax rate is integrated into the combined corporate income tax rate. Previously, including surtax rates challenged interpretation since many surtaxes were only levied on a share of the corporate income.

Individual Taxes

The surtax rate on personal income has been replaced by a dummy variable indicating the existence of surtaxes on personal income. The surtax rate is included in the combined top personal income tax rate, if applicable.

During the production of this year’s report, the OECD table on Top Personal Income Tax Rates (Table I.7) was temporarily disabled due to errors in the data. We took a previous version of that table and made manual corrections using other sources. Social security taxes are included when these aren’t phased out before the top threshold or the combined rate is higher than the top rate.

Corporate Income Tax

The corporate income tax is a direct taxA direct tax is levied on individuals and organizations and cannot be shifted to another payer. Often with a direct tax, such as the personal income tax, tax rates increase as the taxpayer’s ability to pay increases, resulting in what’s called a progressive tax.

on the profits of a corporation. All OECD countries levy a tax on corporate profits, but the tax rates and bases vary significantly across countries. Corporate income taxes reduce the after-tax rate of return on corporate investment. This increases the cost of capital, which leads to lower levels of investment and economic output. Additionally, the corporate tax can lead to lower wages for workers, lower returns for investors, and higher prices for consumers.

Although the corporate income tax has a relatively significant impact on a country’s economy, it raises a relatively low amount of tax revenue for most governments—the OECD average was 9.8 percent of total revenues in 2021.[5]

The ITCI breaks the corporate income tax category into three subcategories. Table 3 displays each country’s Corporate Income Tax category rank and score along with the ranks and scores of the subcategories, namely, the corporate rate, cost recoveryCost recovery is the ability of businesses to recover (deduct) the costs of their investments. It plays an important role in defining a business’ tax base and can impact investment decisions. When businesses cannot fully deduct capital expenditures, they spend less on capital, which reduces worker’s productivity and wages.

, and incentives and complexity.

Combined Top Marginal Corporate Income Tax Rate

The top marginal corporate income tax rate measures the rate at which each additional dollar of taxable profit is taxed. High marginal corporate tax rates tend to discourage capital formation and thus slow economic growth.[6] Countries with higher top marginal corporate income tax rates than the OECD average receive lower scores than those with lower, more competitive rates.

Colombia levies the highest top combined corporate income tax rate, at 35 percent, followed by Portugal (31.5 percent) and Australia, Costa Rica, and Mexico (all at 30 percent). The lowest top marginal corporate income tax rate in the OECD is found in Hungary, at 9 percent, followed by Ireland (12.5 percent) and Lithuania (15 percent). The OECD average combined corporate income tax rate is 23.6 percent for 2023.[7]

Cost Recovery

Business profits are generally determined as revenue (what a business makes in sales) minus costs (the cost of doing business). The corporate income tax is intended to be a tax on these profits. Thus, it is important that a tax code properly defines what constitutes taxable income. If a tax code does not allow businesses to account for all the costs of doing business, it will inflate a business’ taxable income and thus its tax bill. This increases the cost of capital, leading to slower investment and economic growth.

Loss Offset Rules: Carryforwards and Carrybacks

Loss carryover provisions allow businesses to either deduct current year losses against future profits (carryforwards) or deduct current year losses against past profits (carrybacks). Many companies have investment projects with different risk profiles and operate in industries that fluctuate greatly with the business cycle. Carryover provisions help businesses “smooth” their risk and income, making the tax code more neutral across investments and over time.[8]

Ideally, a tax code allows businesses to carry forward their losses for an unlimited number of years, ensuring that a business is taxed on its average profitability over time. While some countries do allow for indefinite loss carryovers, others have time—and deductibility—limits.

In 22 of the 38 OECD countries, corporations can carry forward losses indefinitely in 2023, though 13 of these limit the amount of taxable income that can be offset by losses from previous years.[9] Of the 16 countries with time limits, the average loss carryforward period is eight years. Hungary, Poland, and Slovakia have the most restrictive loss carryover provisions in the OECD: carrybacks are not allowed, and carryforwards are not only limited to five years but also capped at 50 percent of taxable income (coded as 2.5 years).[10] The ITCI ranks countries that allow losses to be carried forward indefinitely without limits better than countries that impose time or deductibility restrictions on carryforwards.

Countries tend to be significantly more restrictive with loss carryback provisions than with carryforward provisions. In 2023, only the Estonian and Latvian systems allow, by design, unlimited carrybacks of losses.[11] Of the nine countries that allow time-limited carrybacks, the average period is 1.3 years.[12] The ITCI penalizes the 27 countries that do not allow any loss carrybacks.

Capital Cost Recovery: Machines, Buildings, and Intangibles

Businesses determine their profits by subtracting costs—such as wages and raw materials—from revenue. However, in most jurisdictions, capital investments—such as in buildings, machinery, and intangibles—are not treated like other regular costs that can be subtracted from revenue in the year the money is spent. Instead, businesses are required to write off these costs over several years or even decades, depending on the type of asset.

DepreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment.

schedules specify the amounts businesses are legally allowed to write off, as well as the time period over which assets need to be written off. For instance, a government may require a business to deduct an equal percentage of the cost of a machine over a seven-year period. By the end of the depreciation period, the business would have deducted the total initial dollar cost of the asset. However, due to the time value of money (a normal real return plus inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power.

), write-offs in later years are not as valuable in real terms as write-offs in earlier years. As a result, businesses effectively lose the ability to deduct the full present value of their investment cost. This tax treatment of capital expenses understates true business costs and overstates taxable income in present value terms.[13]

The ITCI measures a country’s capital allowanceA capital allowance is the amount of capital investment costs, or money directed towards a company’s long-term growth, a business can deduct each year from its revenue via depreciation. These are also sometimes referred to as depreciation allowances.

s for three asset types, namely, machinery, industrial buildings, and intangibles.[14] Capital allowances are expressed as a percent of the present value cost that corporations can write off over the life of an asset. A 100 percent capital allowance represents a business’ ability to deduct the full cost of an investment over its life in real terms. Countries that provide faster write-offs for capital investments receive better scores in the ITCI.

On average, across the OECD, in real terms, businesses can write off 84.9 percent of investment costs in machinery, 48.9 percent of the cost of industrial buildings, and 74.9 percent of the cost of intangibles. In 2023, Chile phased out full expensing for all three asset categories. The policy had been put in place as a response to the COVID-19 pandemic. Similarly, the United Kingdom phased out its 130 percent deduction for machinery and brought in temporary full expensing. The United States phased out full expensing for machinery to an 80 percent expensing allowance. Estonia and Latvia are coded as allowing 100 percent of the present value of a capital investment to be written off, as their corporate tax only applies to distributed profits and is thus determined by cash flow.[15]

Inventories

Similar to capital investments, the costs of inventories are not written off in the year of purchase. Instead, the costs of inventories are deducted at sale. As a result, governments need to define the total cost of inventories sold. There are generally three methods used to calculate inventories: Last In, First Out (LIFO); Average Cost; and First In, First Out (FIFO).

The method by which a country allows businesses to account for inventories can significantly impact a business’ taxable income. When prices are rising, as is usually the case, LIFO is the preferred method because it allows inventory costs to be closer to true costs at the time of sale. This results in the lowest taxable income for businesses. In contrast, FIFO is the least preferred method because it results in the highest taxable income. The Average Cost method is between FIFO and LIFO.[16]

Countries that allow businesses to choose the LIFO method receive the best scores, those that allow the Average Cost method receive an average score, and countries that only allow the FIFO method receive the worst scores. Fourteen OECD countries allow companies to use the LIFO method of accounting, 19 countries use the Average Cost method of accounting, and five countries limit companies to the FIFO method of accounting.[17]

Allowance for Corporate Equity

Businesses can finance their operations through debt or equity. However, the return on these two types of finance is taxed differently. Standard corporate income tax systems allow tax deductionA tax deduction is a provision that reduces taxable income. A standard deduction is a single deduction at a fixed amount. Itemized deductions are popular among higher-income taxpayers who often have significant deductible expenses, such as state/local taxes paid, mortgage interest, and charitable contributions.

s of interest payments but not of equity costs, effectively providing a tax advantage to debt over equity finance—the so-called “debt bias.” This debt bias can be considered a real risk to economic stability.[18]

There are two broad ways to address this debt bias, namely, limiting the tax deductibility of interest and providing a deduction for equity costs. Limiting the tax deductibility of interest expenses creates new distortions, as interest income usually continues to be fully taxed. An allowance for corporate equity—or sometimes also referred to as notional interest deduction—retains the deduction for interest expenses but adds a similar deduction for the normal return on equity, neutralizing the debt bias while eliminating tax distortions to investment.

Five OECD countries—Belgium, Italy, Poland, Portugal, and Turkey—have introduced an allowance for corporate equity.[19] All countries except Poland apply the allowance only to new equity instead of all equity, limiting the tax revenue costs while preserving the efficiency gains. The Belgian policy will be abolished in 2024. The allowance rate is frequently based on the corporate or government bond rate and in some cases is adjusted by a risk premium.[20]

Countries that have implemented an allowance for corporate equity receive a better score in the Index.

Tax Incentives and Complexity

Good tax policy treats economic decisions neutrally, neither encouraging nor discouraging one activity over another. A tax incentive is a tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income, rather than the taxpayer’s tax bill directly.

, deduction, or preferential tax rate that exclusively applies for a specific type of economic activity and can thus distort economic decisions.

For instance, when an industry receives a tax credit for producing a specific product, it may choose to overinvest in that activity, although it might otherwise not be profitable. Additionally, the cost of special provisions is often offset by shifting the burden onto other taxpayers in the form of higher taxes.

In addition, the possibility of receiving incentives invites efforts to secure these tax preferences,[21] such as lobbying, which creates additional deadweight economic loss as firms focus resources on influencing the tax code in lieu of producing products. For instance, the deadweight losses in the United States attributed to tax compliance and lobbying were estimated to be between $215 billion and $987 billion in 2012. These expenditures for lobbying, along with compliance, have been shown to reduce economic growth by crowding out potential economic activity.[22]

The ITCI considers whether countries provide incentives such as patent box provisions and research and development (R&D) tax subsidies. Countries which provide such incentives are scored worse than those that do not.

Patent Boxes

Due to an increasingly globalized and mobile economy, countries have searched for ways to prevent corporations from reincorporating or shifting operations or profits elsewhere. One response to the increase in capital mobility has been the creation of patent boxes.

Patent boxes—also referred to as intellectual property, or IP, regimes—provide tax rates on income derived from IP that are below statutory corporate tax rates. Eligible types of IP are most commonly patents and software copyrights. Patent boxes are an income-based rather than an expenditure-based tax incentive, limiting its benefits to successful R&D projects that have produced IP rights rather than decreasing the ex ante risks of R&D through cost reductions.

Intellectual property is extremely mobile. Hence, a country can use the lower tax rate of a patent box to entice corporations to hold their intellectual property within its borders. Research suggests that patent boxes are likely to attract new income derived from patents, implying that businesses reduce their corporate tax liability by shifting IP-related income. Tax revenues, however, are likely to decline, as the negative revenue effects of the lower statutory rate on patent income can be only partially offset by revenues from newly attracted patent income.[23]

In recent years, patent box rules have become more stringent in some countries as the OECD requirements for countering harmful tax practices have been adopted. Countries that follow the OECD standards now require companies to have substantial R&D activity within their borders to benefit from tax preferences associated with their intellectual property.[24]

Instead of providing patent boxes for intellectual property, countries should recognize that all capital is mobile to some degree and lower their corporate tax rates across the board. This would encourage investment of all kinds, rather than merely incentivizing corporations to locate their patents in a specific country.

Seventeen OECD countries—Australia, Belgium, France, Hungary, Ireland, Israel, Korea, Lithuania, Luxembourg, the Netherlands, Poland, Portugal, Slovakia, Spain, Switzerland, Turkey, and the United Kingdom—have patent box legislation, with rates and exemptions varying among countries.[25] The United States has a reduced tax rate for profits from exports related to intellectual property held in the U.S. which is treated as a patent box in the Index. Countries with patent box regimes receive a lower score.

Research and Development

In the absence of full expensing, expenditure-based R&D tax incentives (partially) offset the tax costs of business investment. Unfortunately, R&D tax incentives are rarely neutral—they usually define very specific activities that qualify—and are often complex in their implementation.

As with other incentives, R&D incentives distort investment decisions and lead to an inefficient allocation of resources.[26] Additionally, the desire to secure R&D incentives encourages lobbying activities that consume resources and detract from investment and production. In Italy, for instance, firms can engage in a negotiation process for incentives, such as easy term loans and tax credits.[27]

Countries could better use the revenue spent on special tax incentives to provide a lower business tax rate across the board or to improve the tax treatment of capital investment.

The implied tax subsidy rate on R&D expenditures, developed by the OECD, measures the extent of expenditure-based R&D tax relief across countries. Implied tax subsidy rates are measured as the difference between one unit of investment in R&D and the pretax income required to break even on that investment unit, assuming a representative firm. In other words, it measures the extent of the preferential treatment of R&D in a given tax system. The more generous the tax provisions for R&D, the higher the implied tax subsidy rates for R&D. An implied subsidy rate of zero means R&D does not receive preferential tax treatment.

Among OECD countries, Colombia has the highest implied tax subsidy rate on R&D expenditures, at 46 percent. Iceland and Portugal provide the second and third most generous relief, with implied tax subsidy rates of 35 and 34 percent, respectively.

Of the countries that grant notable relief, the United States (3 percent), Mexico (6 percent), and Turkey (6 percent) are the least generous. The implied tax subsidy rates of Costa Rica, Estonia, Finland, Israel, Latvia, Luxembourg, and Switzerland do not show any significant expenditure-based R&D tax relief.[28]

Countries that provide more generous expenditure-based R&D tax incentives receive a lower score on the ITCI.

Digital Services Taxes

Over the last few years, several OECD countries have implemented so-called digital services taxes (DSTs). DSTs are taxes on selected gross revenue streams of large digital businesses. Their tax base typically includes revenues either derived from a specific set of digital goods or services (for example, targeted online advertising) or based on the number of digital users within a country. Relatively high domestic and global revenue thresholds limit the tax to large multinationals.

DSTs effectively ring-fence the digital economy by limiting the tax to certain revenue streams of large digital businesses, creating distortions based on firm size and business model. In addition, because DSTs are levied on revenues rather than profits, they do not take into account profitability, and thus disproportionally affect firms with lower profit margins.

As of 2023, eight OECD countries have implemented a DST: Austria, France, Hungary, Italy, Poland, Spain, Turkey, and the United Kingdom.[29]

Countries that have implemented a DST receive a lower score on the ITCI.

Complexity

The ITCI quantifies corporate tax code complexity by measuring the number of separate taxes (and rates) that apply to business income, the existence of surtax rates on business income, and the amount of revenue countries collect from business profits taxes other than the corporate income tax. These burdens are measured by tallying up the separate rates that apply to business income, identifying applicable surtaxes, and relying on OECD revenue data to measure the share of revenue from taxes on business income other than the corporate income tax.

Countries that have multiple rates that apply to corporate income, surtaxes, and collect revenue on income and profits outside of normal income taxes receive worse scores on the ITCI.

The nation with the highest number of separate tax rates is Costa Rica with five. Korea and Portugal follow with four. There are 14 OECD countries that do not have multiple tax rates or bases for their corporate income tax.[30]

Corporate surtaxes are relatively uncommon in OECD countries with just four applying a surtax to business income. Portugal, Luxembourg, Germany, and France all apply a surtax to all or part of their corporate income tax base.[31]

The OECD data on tax revenues has a category for revenues that are unallocable to normal personal or business income taxes.[32] The data show that Chile (10.4 percent), Switzerland (6.4 percent), Denmark (5.4 percent) and Costa Rica (4.9 percent) collect non-negligible shares of revenue from income (including personal income) from taxes other than corporate or personal income taxes. Seventeen OECD countries collect no revenue in that category.

Individual Taxes

Individual taxes are one of the most prevalent means of raising revenue to fund government. Individual income taxes are levied on an individual’s or household’s income (wages and, often, capital gains and dividends) to fund general government operations. These taxes are typically progressive, meaning that the rate at which an individual’s income is taxed increases as the individual earns more income.

In addition, countries have payroll taxes—also referred to as social security contributions or social insurance taxes. These typically flat-rate taxes are levied on wage income in addition to a country’s general individual income tax. However, revenue from these taxes is typically allocated specifically toward social insurance programs such as unemployment insurance, government pension programs, and health insurance.

Individual taxes can have the benefit of being some of the more transparent taxes. Taxpayers are made aware of their total amount of taxes paid at some point in the process—unlike, for example, consumption taxes, which are collected and remitted by a business, and an individual may not be aware of their total consumption tax burden.

Most countries tax individuals on their income using two approaches. First, countries tax earnings from work with ordinary income taxes and payroll taxes. The structure of these taxes can influence individuals’ decisions to work, take an additional part-time job, or whether a second earner in the household will work. Second, individuals are taxed on their savings through taxes on capital gains and dividends. In most cases, these taxes are a second layer of tax on corporate profits and can impact decisions on how much to save and invest. High taxes on capital gains and dividends can reduce the aggregate savings and investment in a country.

A country’s score for its individual income tax is determined by three subcategories: the rate and progressivity of wage taxation, income tax complexity, and the extent to which the income tax double taxes corporate income. Table 4 shows the ranks and scores for the entire Individual Taxes category as well as the rank and score for each subcategory.

Taxes on Ordinary Income

Individual income taxes are levied on the income of individuals or households. Many countries, such as the United States, rely on individual income taxes as a significant source of tax revenue.[33] They are used to raise revenue for both general government operations and for specific programs, such as social insurance and government-provided health insurance.

A country’s taxes on ordinary income are measured according to three variables: the top rate at which ordinary income is taxed, the top income tax threshold, and the economic efficiency of labor taxation.

Top Statutory Personal Income Tax Rate

Most countries’ income tax systems have a progressive taxA progressive tax is one where the average tax burden increases with income. High-income families pay a disproportionate share of the tax burden, while low- and middle-income taxpayers shoulder a relatively small tax burden.

structure. This means that, as individuals earn more income, they move into tax bracketA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat.

s with higher tax rates. The top statutory personal income tax rate is the top tax rate on all income over a certain level. For example, the United States has seven tax brackets, with the seventh (top) bracket taxing each additional dollar of income over $578,125 ($693,750 for married filing jointly) at a rate of 37 percent in 2023.[34] In addition, U.S. taxpayers also pay state and local income taxes, which sum to a combined top combined personal income tax rate of 43.7 percent.[35]

Individuals consider the marginal tax rate when deciding whether to work an additional hour. In many cases the decision will be about taking a second, part-time job or whether households with two adults will have one or two earners. If an individual faces a marginal tax rate of 30 percent on their current earnings, taking additional work or another shift would mean that only 70 percent of those earnings could be brought home.

High top personal tax rates make additional work more expensive, which lowers the relative cost of not working. This makes it more likely that an individual will choose leisure over work, maintaining current hours rather than moving to full-time work or taking an additional shift. High tax rates increase the cost of labor, which can decrease hours worked, and, in turn, can reduce the amount of production in the economy.

Countries with high top statutory personal income tax rates receive a worse score on the ITCI than countries with lower top rates. Slovenia has the highest all-in top statutory personal income tax rate (including employee social contributions) at 67.5 percent. Estonia has the lowest, at 21.6 percent.[36]

Income Level at Which Top Statutory Personal Income Tax Rate Applies

The level at which the top statutory personal income tax rate first applies is also important. If a country has a top rate of 20 percent, but almost everyone pays that rate because it applies to any income over $10,000, that country essentially has a flat income tax. In contrast, a tax system that has a top rate that applies to all income over $1 million requires a much higher top tax rate to raise the same amount of revenue, because it targets a small number of people that earn a high level of income.

Countries with top statutory personal income tax rates that apply at lower levels score better on the ITCI. The ITCI bases its measure on the income level at which the top rate first applies as compared to the country’s average income. According to this measure, Mexico applies its top tax rate at the highest level of income (the top personal income tax rate applies at 25.2 times the average Mexican income), whereas Hungary applies its top rate on the first dollar, with a flat personal income tax of 15 percent.[37]

The Economic Cost of Labor Taxation

All taxes create some economic losses; however, tax systems should be designed to minimize those losses while supporting revenue needs.

One way to examine the efficiency of labor taxation in a country is to control for the level of labor taxation using the ratio of the marginal tax wedgeA tax wedge is the difference between total labor costs to the employer and the corresponding net take-home pay of the employee. It is also an economic term that refers to the economic inefficiency resulting from taxes.

to the average tax wedge.[38] The marginal tax wedge influences the choice to earn another dollar of income while the average tax wedge measures the tax burden at the current income level.[39] A higher ratio means that as one earns more income, the influence of the tax system on those decisions and the related economic losses grows. A lower ratio means that an individual can decide to work more without the tax system changing their decisions.

For example, one individual faces an average tax wedge on their earnings of 20 percent and their marginal tax wedge is also 20 percent. That individual could work more hours without the relative tax burden growing. The ratio of that worker’s marginal tax wedge to their average tax wedge is 1. Another individual who faces an average tax wedge of 20 percent on their earnings and a marginal tax wedge of 30 percent, however, would have their decision of whether to work more hours influenced by the tax system. The ratio of that worker’s marginal tax wedge to their average tax wedge is 1.5.

The ITCI gives countries with high ratios a worse score due to the larger impact that those systems have on workers’ decisions.

Hungary has the lowest ratio of 1, meaning the next dollar earned faces the same tax burden as current earnings.[40] This is because Hungary has a flat income tax, so the marginal and average tax wedge are the same. In contrast, in Israel, the ratio is 1.6. The average across OECD countries is 1.54.[41]

Complexity

Complexity is measured by the rate of any surtax on personal income and the amount of revenue raised through social security contributions other than those collected through employer or employee payroll taxes. These measures indicate non-standard approaches to taxation of labor income and, in the case of surtaxes, a less transparent personal income tax system. The Index penalizes countries with surtaxes and significant revenues from non-standard employer and employee payroll taxes.

Four OECD countries levy a surtax on personal income: Germany, Japan, Korea, and Luxembourg. Germany levies a 5.5 percent solidarity surcharge on income tax paid in excess of EUR 17,539, equivalent to labor income above EUR 65,500 for single filers, increasing its top marginal income tax rate from 45 percent to 47.475 percent. Japan applies a 2.1 percent surtax on all national (but not local) income tax liability.

Four OECD countries raise some meaningful share of revenue through non-standard social security contributions. In Costa Rica, these revenues make up 28.9 percent of total tax revenues. Mexico (14 percent), Colombia (10 percent), and Iceland (8.5 percent) make up the others in this group.

Capital Gains and Dividends Taxes

In addition to wage income, many countries’ individual income tax systems tax investment income by levying taxes on capital gains and dividends.

A capital gain occurs when an individual purchases an asset (usually corporate stock) in one period and sells it in another for a profit. A dividend is a payment made to an individual from after-tax corporate profits.

Capital gains taxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. Capital gains taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment.

es and personal dividend taxes are a form of double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income.

of corporate profits that contribute to the tax burden on capital. When a corporation makes a profit, it pays corporate income tax. It can then generally do one of two things. The corporation can retain the after-tax profits, which boost the value of the business and thus its stock price. Stockholders then sell the stock and realize a capital gain, which requires them to pay tax on that income. Alternatively, the corporation can distribute the after-tax profits to shareholders in the form of dividends. Stockholders who receive dividends then pay dividends tax on that income.

A company that makes a taxable profit of $1 million and pays 20 percent in corporate income taxes would have $800,000 left to either reinvest in the company, which would boost the value of the stock, or pay a dividend. A shareholder might face an additional 20 percent tax on the gains from selling the shares or on a dividend from the company. Effectively, the system taxes the business profits at 36 percent. An individual hoping that an investment provides a 10 percent real rate of return might see only a 6.4 percent after-tax rate of return.

Some tax systems account for this potential double taxation either through credits against capital gains taxes for corporate taxes paid or other deductions. Such a tax system provides integrated taxation of corporate profits, or “corporate integration.”[42]

Apart from double taxation, taxes on dividends and capital gains can change the incentives for businesses when they are looking to finance new projects. If a business can either fund a new project through selling new shares of stock or through reinvesting its profits, the taxes on investors can influence which approach results in higher after-tax returns. Norway uses a rate of return allowance on capital gains taxes to neutralize the decision between reinvesting profits or selling new shares.[43]

Generally, higher dividends and capital gains taxes create a bias against saving and investment, reduce capital formation, and slow economic growth.[44]

In the ITCI, a country receives a better score for lower capital gains and dividends taxes.

Capital Gains Tax Rates

Countries generally tax capital gains at a lower rate than ordinary income, provided that specific requirements are met. For example, the United States taxes capital gains at a reduced rate if the taxpayer holds the asset for at least one year before selling it (so-called long-term capital gains).[45] The ITCI gives countries with higher capital gains tax rates a worse score than those with lower rates.

Some countries use additional provisions to help mitigate the double taxation of income due to the capital gains tax. For instance, the United Kingdom provides an annual exemption of EUR 6,000 (USD 7,400),[46] and Canada excludes half of all capital gains income from taxation.[47]

Denmark has the highest capital gains tax rate in the OECD, at 42 percent. Belgium, the Czech Republic, Korea, Luxembourg, New Zealand, Slovakia, Slovenia, Switzerland, and Turkey do not tax long-term capital gains.[48]

Dividend Tax Rates

Dividend taxes can adversely impact capital formation in a country. High dividend tax rates increase the cost of capital, which deters investment and slows economic growth.

Countries’ rates are expressed as the top marginal personal dividend tax rate after any imputation or credit system.

Countries with lower overall dividend tax rates score better on the ITCI due to the dividend tax rate’s effect on the cost of investment (i.e., the cost of capital) and the more neutral treatment between saving and consumption. Ireland has the highest dividend tax rate in the OECD, at 51 percent. Estonia and Latvia have dividend tax rates of 0 percent due to their cash-flow corporate tax system, and Colombia’s top dividend tax rate is 0. The OECD average is 24 percent.[49]

Consumption Taxes

Consumption taxes are levied on individuals’ purchases of goods and services. In the OECD and most of the world, the value-added tax (VAT)A Value-Added Tax (VAT) is a consumption tax assessed on the value added in each production stage of a good or service. Every business along the value chain receives a tax credit for the VAT already paid. The end consumer does not, making it a tax on final consumption.

is the most common general consumption tax.[50] Most general consumption taxes either do not tax intermediate business inputs or allow a credit for taxes already paid on them, making them one of the most economically efficient means of raising tax revenue.

However, many countries define their tax base inefficiently. Most countries levy reduced tax rates and exempt certain goods and services from VAT, requiring them to levy higher standard tax rates to raise sufficient revenue. Some countries fail to properly exempt business inputs. For example, states in the United States often levy sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding.

es on machinery and equipment.[51]

A country’s consumption tax score is broken down into three subcategories: the tax rate, the tax base, and complexity. Table 5 displays the ranks and scores for the Consumption Taxes category.

Consumption Tax Rate

If levied at the same rate and properly structured, a VAT and a retail sales tax will each raise approximately the same amount of revenue. Ideally, either a VAT or a sales tax should be levied at the standard rate on all final consumption (although they are implemented in slightly different ways). With a sufficiently broad consumption tax base, the tax rate can be relatively low. A VAT or retail sales tax with a low rate and neutral structure limits economic distortions while raising substantial revenue.

However, many countries have consumption taxes that exempt certain goods and services from VAT or tax them at a reduced rate, requiring higher standard rates to raise sufficient revenue. If not neutrally structured, high tax rates create economic distortions by discouraging the purchase of highly taxed goods and services in favor of untaxed, lower taxed, or self-provided goods and services.

Countries with lower consumption tax rates score better than those with higher tax rates, as lower rates do less to discourage economic activity and allow for more future consumption and investment.

The average general consumption tax rate in the OECD is 19.0 percent. Hungary has the highest tax rate at 27 percent, while the United States has the lowest tax rate at 7.4 percent.[52]

Consumption Tax Base

Ideally, either a VAT or a sales tax should be levied at a standard rate on all final consumption. In other words, consumption tax collections should be equal to the amount of final consumption in the economy times the rate of the sales tax or VAT. However, many countries’ consumption tax bases are far from this ideal. Many countries exempt certain goods and services from the VAT or tax them at a reduced rate, requiring a higher standard rate than would otherwise be necessary, or apply the tax to business inputs, increasing the cost of capital.

VAT/Sales Tax ExemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the IRS, preventing them from having to pay income tax.

Threshold

Most OECD countries set exemption thresholds for their VATs/sales taxes. If a business is below a certain annual revenue threshold, it is not required to participate in the VAT system. This means that small businesses—unlike businesses above that threshold—do not collect VAT on their outputs sold to customers but also cannot receive a refund for VAT paid on business inputs.[53] Although exempting very small businesses saves administrative and compliance costs, unnecessarily large thresholds create a distortion by favoring smaller businesses over larger ones.

Countries receive better scores for lower thresholds. The United Kingdom receives the worst threshold score with a VAT threshold of $123,188.[54] Seven countries receive the best scores for having no general VAT/sales tax exemption threshold (Chile, Colombia, Costa Rica, Mexico, Spain, Turkey, and the United States). The average across the OECD countries that have a VAT threshold is approximately $57,500.[55]

Consumption Tax Base as a Percent of Total Consumption

One way to measure a country’s VAT base is the VAT revenue ratio. This ratio looks at the difference between the VAT revenue actually collected and collectable VAT revenue under a VAT that was applied at the standard rate on all final consumption. The difference in actual and potential VAT revenues is due to 1) policy choices to exempt certain goods and services from VAT or tax them at a reduced rate, and 2) lacking VAT compliance.[56]

For example, if final consumption in a country is $100 and a country levies a 10 percent VAT on all goods and services, a pure base would raise $10. Revenue collection below $10 reflects either a high number of exemptions or reduced rates built into the tax code or low levels of compliance (or both). The base is measured as a ratio of the pure base collections to the actual collections. Countries with tax base ratios near 1—signifying a pure tax base—score better.

Under this measure, New Zealand has the broadest tax base covering approximately 100 percent of total consumption. Luxembourg and Estonia follow with ratios of 0.86 and 0.78, respectively. Greece (0.36), the United States (0.36), and Colombia (0.37) have the worst ratios. The OECD average tax base ratio is 0.58.[57]

Property Taxes

Property taxes are government levies on the assets of an individual or business. The methods and intervals of collection vary widely among the types of property taxes. Estate and inheritance taxAn inheritance tax is levied upon an individual’s estate at death or upon the assets transferred from the decedent’s estate to their heirs. Unlike estate taxes, inheritance tax exemptions apply to the size of the gift rather than the size of the estate.

es, for example, are due upon the death of an individual and the passing of his or her estate to an heir, respectively. Taxes on real property, on the other hand, are paid at set intervals–often annually–on the value of taxable property such as land and real estate.

Many types of property taxes are highly distortive and add significant complexity for taxpayers. Estate and inheritance taxes create disincentives against additional work and saving, which damages productivity and output. Financial transaction taxes increase the cost of capital, which limits the flow of investment capital to its most efficient allocations.[58] Taxes on wealth limit the capital available in the economy, which damages long-term economic growth and innovation.[59]

Sound tax policy minimizes economic distortions. Except for taxes on land, most property taxes increase economic distortions and have long-term negative effects on the economy and its productivity.

Table 6 shows the ranks and scores for the Property Taxes category and each of its subcategories, which are real property taxes, wealth and estate taxAn estate tax is imposed on the net value of an individual’s taxable estate, after any exclusions or credits, at the time of death. The tax is paid by the estate itself before assets are distributed to heirs.

es, and capital and transaction taxes.

Real Property Taxes

Real property taxes are levied on a recurrent basis on taxable property. For example, in most states or municipalities in the United States, businesses and individuals pay a property tax based on the value of their real property.

Structure of Property Taxes

Although taxes on real property are generally an efficient way to raise revenue, some real property taxes can become direct taxes on capital. This occurs when a tax applies to more than just the value of the land itself, such as the buildings or structures on the land. This increases the cost of capital, discourages the formation of capital (such as the building of structures), and can negatively impact business location decisions.

When a business wants to improve its property through renovations or expanding a factory, a property tax that applies to both the land and those improvements directly increases the costs of those improvements. However, a tax that just applies to the value of the land would not create an incentive against property improvements.

Countries that tax the value of structures and buildings as well as land receive the worst scores on the ITCI. Some countries mitigate this treatment with a deduction for property taxes paid against corporate taxable income. These countries receive slightly better scores. Countries receive the best possible score if they have either no property tax or only tax land.

Every OECD country except Australia andEstoniaapplies its property tax to all capital (land and buildings/structures).[60] These two countries only tax the value of land, which excludes the value of any buildings or structures on the land. Of the 35 OECD countries with taxes on all capital, 30 allow for a deduction against corporate taxable income.[61]

Real Property Tax Collections

The variable “property tax collections” measures property tax revenues as a percent of a country’s private capital stock. Higher tax burdens, specifically when on capital, tend to slow investment, which damages productivity and economic growth.

Countries with a high level of collections as a percent of their capital stock place a larger tax burden on taxpayers and receive a worse score on the ITCI. Seven countries in the OECD have property tax collections that are greater than 1 percent of the private capital stock. Leading this group are the United Kingdom (1.8 percent), the United States (1.7 percent), and Canada (1.6 percent). Austria, the Czech Republic, Luxembourg, Mexico, and Switzerland have a real property tax burden of below 0.1 percent of the private capital stock.[62]

Wealth and Estate Taxes

Many countries also levy property taxes on an individual’s wealth. These taxes can take the form of estate or inheritance taxes that are levied either upon an individual’s estate at death or upon the assets transferred from the decedent’s estate to the heirs. These taxes can also take the form of a recurring tax on an individual’s wealth. Estate and inheritance taxes limit resources available for investment or production and reduce the incentive to save and invest.[63] This reduction in investment adversely affects economic growth. Moreover, these taxes, the estate and inheritance tax especially, can be avoided with certain planning techniques, which makes the tax an inefficient and unnecessarily complex source of revenue.

Wealth Taxes

In addition to estate and inheritance taxes, some countries levy wealth taxes. Wealth taxes are often low-rate, progressive taxes on an individual’s or family’s assets or the assets of a corporation. Unlike estate taxes, wealth taxes are levied on an annual basis. While some countries levy a comprehensive tax on net wealth, others limit their wealth taxes to selected assets, such as security accounts, financial assets held abroad, or real estate.

Four countries levy net wealth taxes, namely Colombia, Norway, Spain, and Switzerland. Belgium, France, and Italy impose wealth taxes on selected assets. Countries with no type of wealth tax receive the best score, countries with wealth taxes on selected assets receive an average score, and countries with net wealth taxes receive the lowest score.[64]

Estate, Inheritance, and Gift TaxA gift tax is a tax on the transfer of property by a living individual, without payment or a valuable exchange in return. The donor, not the recipient of the gift, is typically liable for the tax.

es

Estate taxes are levied on the value of an individual’s taxable estate at the time of death and are paid by the estate itself, while inheritance taxes are levied on the value of assets transferred to an individual’s heirs upon death and are paid by the heirs (not the estate of the deceased individual). Gift taxes are taxes on the transfer of property (cash, stocks, and other property) that are typically used to prevent individuals from circumventing estate and inheritance taxes by gifting away their assets before death.

Rates, exemption levels, and rules vary substantially among countries. For example, the United States levies a top rate of 40 percent on estates but has an exemption level of $12.92 million. Belgium’s Brussels capital region, on the other hand, has an inheritance tax with an exemption of EUR 15,000 (USD 14,270)[65] and a variety of tax rates depending on who receives assets from the estate and what the assets are.[66]

Estate, inheritance, and gift taxes create significant compliance costs for taxpayers while raising insignificant amounts of revenue. According to OECD data for 2021, estate, inheritance, and gift taxes across the OECD raised an average of 0.15 percent of GDP in tax revenue, with the highest amount raised being only 0.74 percent of GDP in France, despite France’s top inheritance tax rate of up to 60 percent in some cases.[67]

Countries without these taxes score better than countries that have them. Thirteen countries in the OECD have no estate, inheritance, or gift taxes: Australia, Austria, Canada, Colombia, Costa Rica, Estonia, Israel, Latvia, Mexico, New Zealand, Norway, Slovakia, and Sweden. All others levy an estate, inheritance, or gift tax.[68]

Capital, Wealth, and Property Taxes on Businesses

There are various taxes countries levy on the assets and fixed capital of businesses. These include taxes on the transfer of real property, taxes on the net assets of businesses, taxes on raising capital, and taxes on financial transactions. These taxes contribute directly to the cost of capital for businesses and reduce the after-tax rate of return on investment.

Property Transfer Taxes

Property transfer taxes are taxes on the transfer of real property (real estate, land improvements, machinery) from one person or firm to another. A common example in the United States is the real estate transfer tax, which is commonly levied at the state level on the value of homes that are purchased by individuals.[69] Property transfer taxes represent a direct tax on capital and increase the cost of purchasing property.

Countries receive a worse score if they have property transfer taxes. Six OECD countries do not have property transfer taxes: Chile, the Czech Republic, Estonia, Lithuania, New Zealand, and Slovakia.[70]

Corporate Asset Taxes

Similar to wealth taxes, asset taxes are levied on the wealth, or assets, of a business. For instance, Luxembourg levies a 0.5 percent tax on the worldwide net wealth of nontransparent Luxembourg-based companies every year.[71] Similarly, cantons in Switzerland levy taxes on the net assets of corporations, varying from 0.001 percent to 0.5 percent of corporate net assets.[72] Other countries levy these taxes exclusively on bank assets.

Nineteen OECD countries have some type of corporate wealth or asset tax. Fourteen of these countries have bank taxes of some type.[73]

Capital Duties

Capital duties are taxes on the issuance of shares of stock. Typically, countries either levy these taxes at very low rates or require a small, flat fee. For example, Switzerland requires resident companies to pay a 1 percent tax on the issuance of shares of stock.[74] These types of taxes increase the cost of capital, limit funds available for investment, and make it more difficult to form businesses.[75]

Countries with capital duties score worse than countries without them. Ten countries in the OECD levy some type of capital duty.[76]

Financial Transaction Taxes

A financial transaction tax is a levy on the sale or transfer of a financial asset. Financial transaction taxes take different forms in different countries. Finland levies a tax of 1.6 percent on the transfer of Finnish securities. On the other hand, Poland levies a 1 percent stamp duty on exchanges of property rights based on the transaction value. For transactions on a stock exchange, the tax is the responsibility of the buyer.[77]

Financial transaction taxes impose an additional layer of taxation on the purchase or sale of stocks. Markets run on efficiency, and capital needs to flow quickly to its most economically productive use. A financial transaction tax impedes this process.[78]

The ITCI ranks countries with financial transaction taxes worse than countries without them. Fourteen countries in the OECD have financial transaction taxes, including France and the United Kingdom, while 24 countries do not impose financial transaction taxes.[79]

Cross-Border Tax Rules

In an increasingly globalized economy, businesses often expand beyond the borders of their home countries to reach customers and build supply chains around the world. Countries have defined rules that determine how, or if, corporate income earned in foreign countries is taxed domestically. Cross-border tax rules comprise the systems and regulations that countries apply to those business activities.

There has been a growing trend of moving from worldwide taxation toward a system of territorial taxation, in which a country’s corporate tax is limited to profits earned within its borders.[80] In a pure territorial tax system, corporations only pay taxes to the country in which they earn income. Since the 1990s, the number of OECD countries with worldwide tax systemA worldwide tax system for corporations, as opposed to a territorial tax system, includes foreign-earned income in the domestic tax base. As part of the 2017 Tax Cuts and Jobs Act (TCJA), the United States shifted from worldwide taxation towards territorial taxation.

s has dropped from more than 20 to a handful.[81]

As part of the Tax Cuts and Jobs Act in December 2017, the United States adopted a hybrid international tax system. Foreign-sourced dividends are now exempt from domestic taxation, but base erosion rules are now stronger and more complex.[82]

The new U.S. system has three pieces: Global Intangible Low-Tax Income (GILTI), Foreign Derived Intangible Income (FDII), and the Base Erosion and Anti-Abuse Tax (BEAT)The Base Erosion and Anti-Abuse Tax (BEAT) was adopted as part of the 2017 tax reform bill and is a tax meant to prevent foreign and domestic corporations operating in the United States from avoiding domestic tax liability by shifting profits out of the United States.

. GILTI liability is effectively a 10.5 percent minimum tax on supra-normal returns derived from certain foreign investments earned by U.S. companies. FDII is designed to be a reduced rate on exports of U.S. companies connected to intellectual property located in the U.S. Effectively, FDII earnings are taxed at 13.125 percent. Paired together, GILTI and FDII create a worldwide tax on intangible income.

The BEAT is designed as a 10 percent minimum tax (initially 5 percent in 2018) on U.S.-based multinationals with gross receipts of $500 million or more. The tax applies to payments by those large multinationals if payments to CFCs exceed 3 percent (2 percent for certain financial firms) of total deductions taken by a corporation.

The proposal for a global minimum tax will dramatically change the landscape for cross-border tax rules. Many OECD countries are proceeding to implement the global minimum tax rules, including the 27 EU Member States, the United Kingdom, Japan, Korea, and Australia. Nonetheless, those rules will not be in place until 2024 at the earliest.[83]

Table 7 displays the overall rank and score for the Cross-Border Tax Rules category as well as the ranks and scores for the subcategories—which include a category for dividends and capital gains exemptions (territoriality), withholdingWithholding is the income an employer takes out of an employee’s paycheck and remits to the federal, state, and/or local government. It is calculated based on the amount of income earned, the taxpayer’s filing status, the number of allowances claimed, and any additional amount of the employee requests.

taxes, tax treaties, and anti-tax avoidance rules.

Territoriality

Under a territorial tax system, multinational businesses pay taxes to the countries in which they earn their income. This means that territorial tax regimes do not generally tax corporate income companies earn in foreign countries. A worldwide tax system—such as the system previously employed by the United States—requires companies to pay taxes on worldwide income, regardless of where it is earned. Several countries—as is now the case in the U.S.—operate some sort of hybrid system.

Countries enact territorial tax systems through so-called “participation exemptions,” which include full or partial exemptions for foreign-earned dividend or capital gains income (or both). Participation exemptions eliminate the additional domestic tax on foreign income by allowing companies to ignore—some or all—foreign income when calculating their taxable income. A pure territorial system fully exempts foreign-sourced dividend and capital gains income.

Companies based in countries with worldwide tax systems are at a competitive disadvantage because they face potentially higher levels of taxation than their competitors based in countries with territorial tax systems. Additionally, taxes on repatriated corporate income in a company’s home country increase complexity and discourage investment and production.[84]

The territoriality of a tax system is measured by the degree to which a country exempts foreign-sourced income through dividend and capital gains exemptions.

Dividends Received Exemption

When a foreign subsidiary of a parent company earns income, it pays corporate income tax to the country in which it does business. After paying the tax, the subsidiary can either reinvest its profits into ongoing activities (by purchasing equipment or hiring more workers, for example) or it can distribute its profits back to the parent company in the form of dividends.

Under a worldwide tax system, the dividends received by a parent company are taxed again by the parent company’s home country, minus a tax credit for taxes already paid on that income. Under a pure territorial system, those dividends are exempt from taxation in the parent’s country.

Countries receive a score based on the level of dividend exemption they provide. Countries with no dividend exemption (worldwide tax systems) receive the worst score.

Twenty-six OECD countries exempt all foreign-sourced dividends received by parent companies from domestic taxation. Eight countries allow 95 percent or 97 percent of foreign-sourced dividends to be exempt from domestic taxation. Four OECD countries have a worldwide or hybrid tax system that generally does not exempt foreign-sourced dividends from domestic taxation.[85]

Branch or Subsidiary Capital Gains Exclusion

Another feature of an international tax system is its treatment of capital gains earned through foreign investments. When a parent company invests in a foreign subsidiary (i.e., purchases shares in a foreign subsidiary), it can realize a capital gain on that investment if it later divests the asset. A territorial tax system would exempt these gains from domestic taxation, as they are derived from overseas activity.

Taxing foreign-sourced capital gains income at domestic tax rates can discourage saving and investment.

Countries that exempt foreign-sourced capital gains from domestic taxation receive a better score on the ITCI. Foreign-sourced capital gains are fully excluded from domestic taxation in 25 OECD countries. Six countries partially exclude foreign-sourced capital gains. Seven countries do not exclude foreign-sourced capital gains income from domestic taxation.[86]

Restrictions on Eligible Countries

An ideal territorial system would only concern itself with the profits earned within the home country’s borders. However, many countries have restrictions on their territorial systems that determine when a business’ dividends or capital gains received from foreign subsidiaries are exempt from domestic tax.

Some countries treat foreign corporate income differently depending on the country in which the foreign income was earned. For example, several countries restrict their territorial systems based on a “blacklist” of countries that do not follow certain requirements. Among EU countries, it is common to restrict the participation exemption to member states of the European Economic Area.

The eligibility rules create additional complexity for companies and are often established in an arbitrary manner. Portugal, for instance, limits exemptions for foreign-sourced dividends and capital gains to those earned in countries that are not listed as a tax haven and that impose an income tax listed in the EU parent-subsidiary directive or have an income tax equal to at least 60 percent of the Portuguese corporate tax rate.[87] Italy, which normally allows a 95 percent tax exemption for foreign-sourced dividends paid to Italian shareholders, does not allow the exemption if the income was earned in a subsidiary located in a blacklisted country, unless evidence that an adequate level of taxation was borne by the foreign entity can be provided.[88]

In the OECD, 20 of 35 countries that provide participation exemptions place restrictions on whether they exempt foreign-sourced income from domestic taxation based on the source country of the income.[89] Countries that have these restrictions on their territorial tax systems receive a worse score on the ITCI.

Withholding Taxes

When firms pay dividends, interest, and royalties to foreign investors or businesses, governments often require those firms to withhold a certain portion to pay as tax. For example, the United States requires businesses to withhold a maximum 30 percent tax on dividends, interest, and royalty payments to foreign individuals unless a tax treaty provides otherwise.

These taxes make investment more costly both for investors, who will receive a lower return on dividends, and for firms, that must pay a higher amount in interest or royalty payments to compensate for the cost of the withholding taxes. These taxes also reduce funds available for investment and production and increase the cost of capital.

Countries with higher withholding tax rates on dividends, interest, and royalties score worse in the ITCI. Dividends, interest, and royalties from these countries do not always face the same tax rate as when distributed to domestic shareholders. Tax treaties between countries either reduce or eliminate withholding taxes.

Chile and Switzerland levy the highest dividend and interest withholding rates, requiring firms to withhold 35 percent of a dividend or interest payment paid to foreign entities or persons. Meanwhile, Estonia, Hungary, and Latvia do not levy withholding taxes on dividends or interest payments.

For royalties, Mexico requires firms to retain the highest amount, at 35 percent, followed by Australia, Belgium, and the United States, at 30 percent. Hungary, Latvia, Luxembourg, the Netherlands, Norway, Sweden, and Switzerland do not require companies to retain any amount of royalties for withholding tax purposes.[90]