Capital investment is critical for driving innovation and sustainable economic growth. Unfortunately, some countries’ important investment incentives are scheduled to decrease in the coming years—including in three countries that account for nearly a fifth of global private investment. Policymakers have an opportunity to support long-term growth by making these policies permanent.

When businesses make investments in physical assets, they consider how profitable a new production facility or machine might be. One factor that impacts profitability is the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

treatment of investment costs. If investment costs can be immediately deducted, then the business is able to make the investment without worrying about inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power.

eroding its deductible costs. However, most countries require businesses to deduct costs over time—in some cases decades—which raises the after-tax cost of making an investment by eroding the value of deductions.

The rules that specify how much of an investment can be deducted each year are called depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment.

schedules, and the amount to be deducted is called a capital allowanceA capital allowance is the amount of capital investment costs, or money directed towards a company’s long-term growth, a business can deduct each year from its revenue via depreciation. These are also sometimes referred to as depreciation allowances.

.

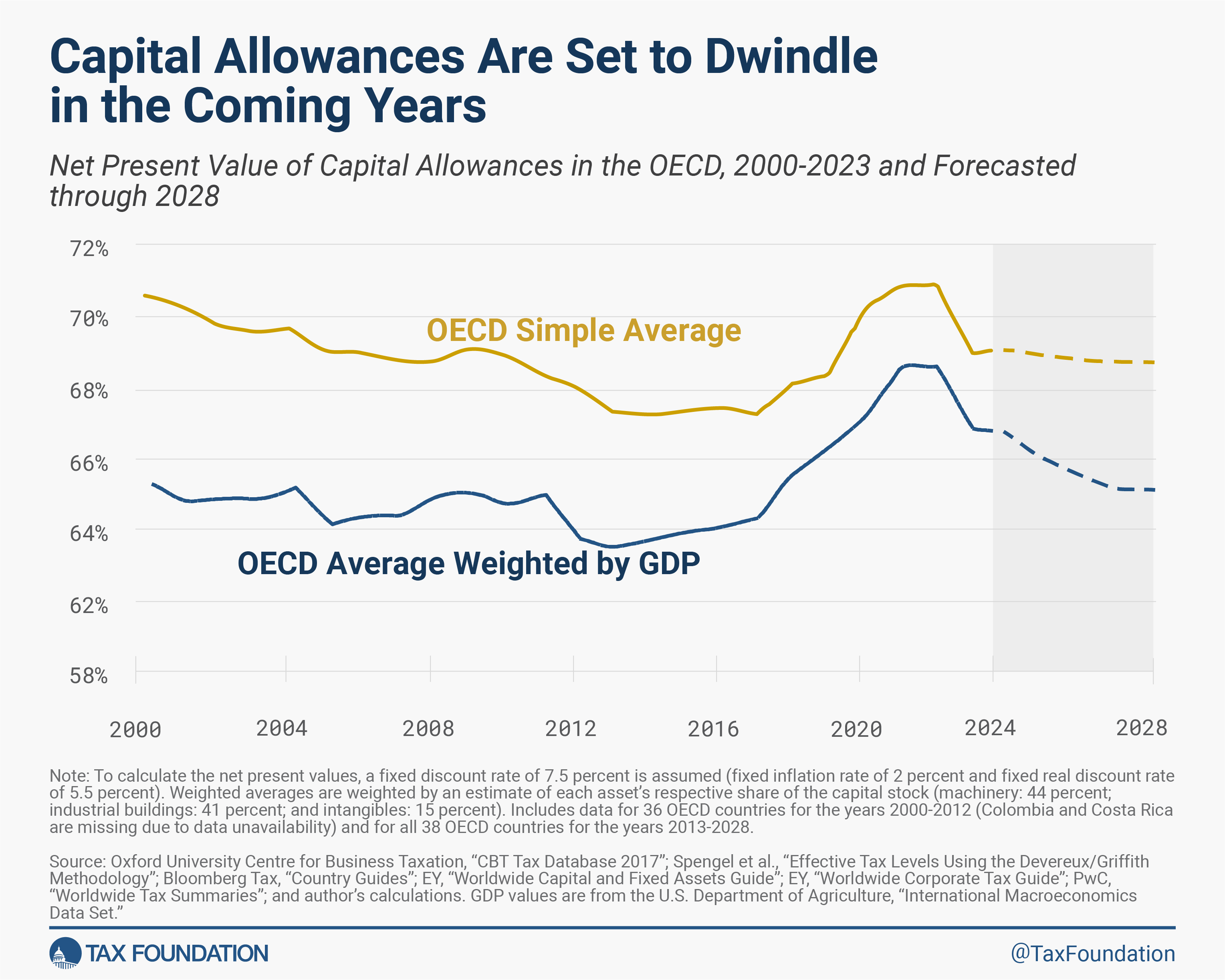

Our recent report on capital allowances in developed countries shows that on average, in 2022, the 38 countries in the Organisation for Economic Co-operation and Development (OECD) provided businesses with the ability to deduct only 70.7 percent of their investment costs over time. The calculation accounts for the time value of money, which is impacted by inflation.

Additionally, in high-inflation scenarios like the current one—where the OECD annual inflation was 9.6 percent in 2022—the investment amount businesses can recover is significantly diminished. An increase in inflation from 2 percent to 9.5 percent reduces the investment costs businesses can recover by up to 15 percentage points. On average, 44.2 percent of investment costs would not be deductible in OECD countries.

In 2022, some countries had provisions to allow businesses to deduct the full costs of investment, including Chile, Estonia, and Latvia. Other countries, including Canada, the United Kingdom, and the United States, provided full deductions for certain investments in equipment.

The impact of these reforms can be seen through the lens of this year’s International Tax Competitiveness Index. Partly thanks to improved capital allowances, over the past 10 years, Canada’s final rank increased by 12 places from 27th to 15th, the United States’ rank rose by 9 places from 30th to 21st, and Finland improved its rank by 7 places from 26th to 19th. In contrast, Chile’s final rank dropped by 4 places from 31st to 35th in the past year, as its full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs.

regime phased out completely.

Unfortunately, some of these policies are temporary. As the policies expire, the after-tax cost of investment will rise. The amount of investment costs that businesses can deduct took a steep fall from 70.7 percent (68.7 percent when weighting the data by GDP) in 2022 to 68.7 percent (66.9 percent weighted) in 2023. From 2023 to 2028, as more policies are set to phase out, capital allowances are expected to dwindle further to 68.4 percent (65.1 percent weighted). The decline of capital allowances in the United States accounts for most of the sharper decline in the weighted average.

Chile’s temporary full expensing for all assets implemented in 2020 already expired at the end of 2022, drastically moving the country’s system of capital allowances from one of the best to the worst in the OECD.

In Canada, a policy that provides immediate deductions for investments in equipment will begin phasing out in 2024 until it fully expires after 2027. The policy was first put in place in 2018.

In the United States, bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings, in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs.

, which was adopted in 2017, is phasing out in 2023. By 2027, the treatment of business investment will return to a much less generous policy.

In Germany, accelerated depreciation schedules for machinery were in place for the years 2020-2022. While the federal government intends to resume them for 2024 as part of the Growth Opportunities Act, the provisions are set to expire by 2025 if not renewed.

Countries like the United Kingdom and Finland, on the other hand, recognized the importance of capital allowances in supporting business investment and decided to prolong or modify the policies set to expire.

In the United Kingdom, the temporary super-deductionA super-deduction is a tax deduction that permits businesses to deduct more than 100 percent of their eligible expenses from their taxable income. As such, the super-deduction is effectively a subsidy for certain costs. This policy sometimes applies to capital costs or research and development (R&D) spending.

of 130 percent for equipment that expired at the end of March 2023 was substituted by full expensing. Additionally, long-life asset investments are subject to a 50 percent first-year deduction. In his Autumn Statement, British Chancellor Jeremy Hunt confirmed that full expensing will be made permanent instead of expiring on March 31, 2026. The change is expected to raise long-run GDP by 0.9 percent, investment by 1.5 percent, and wages by 0.8 percent, relative to a return to the pre-2021 law.

In Finland, the declining balance depreciation rate for machinery was temporarily doubled for the years 2020-2023. A proposal to extend the increased depreciation rules to 2025 was recently approved.

While a permanent expansion of capital allowances would support business investment, capital formation, and economic growth over the long term, temporary expansions have much more limited impacts. Businesses may accelerate some investment decisions they had already planned, but that just changes the timing for when investments happen rather than increasing the level of investment overall.

The policies in Canada, Germany, and the U.S. are particularly important. In 2019, the four countries accounted for more than 20 percent of worldwide private investment. If their policies are not geared toward investment, it will put a drag on worldwide investment and economic output.

Rather than adopt temporary policies that phase out and expire, policymakers should focus their efforts on long-term reforms to support investment. In fact, Canada, Germany, and the U.S. should aim to permanently provide immediate deductions for investments in machinery and equipment, and for all other capital investments, they should provide adjustments for inflation and the time value of money.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Share