As lawmakers prepare for the debate over the expiration of the 2017 TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

Cuts and Jobs Act (TCJA), they may face increasing pressure to offset the cost of lowering tax rates by changing other parts of the tax code. One potential option to raise additional revenue to cover the cost of the TCJA’s reforms—like lower rates, a larger standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. It was nearly doubled for all classes of filers by the 2017 Tax Cuts and Jobs Act (TCJA) as an incentive for taxpayers not to itemize deductions when filing their federal income taxes.

, and a larger child tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income, rather than the taxpayer’s tax bill directly.

—would be to repeal the head of household filing status.

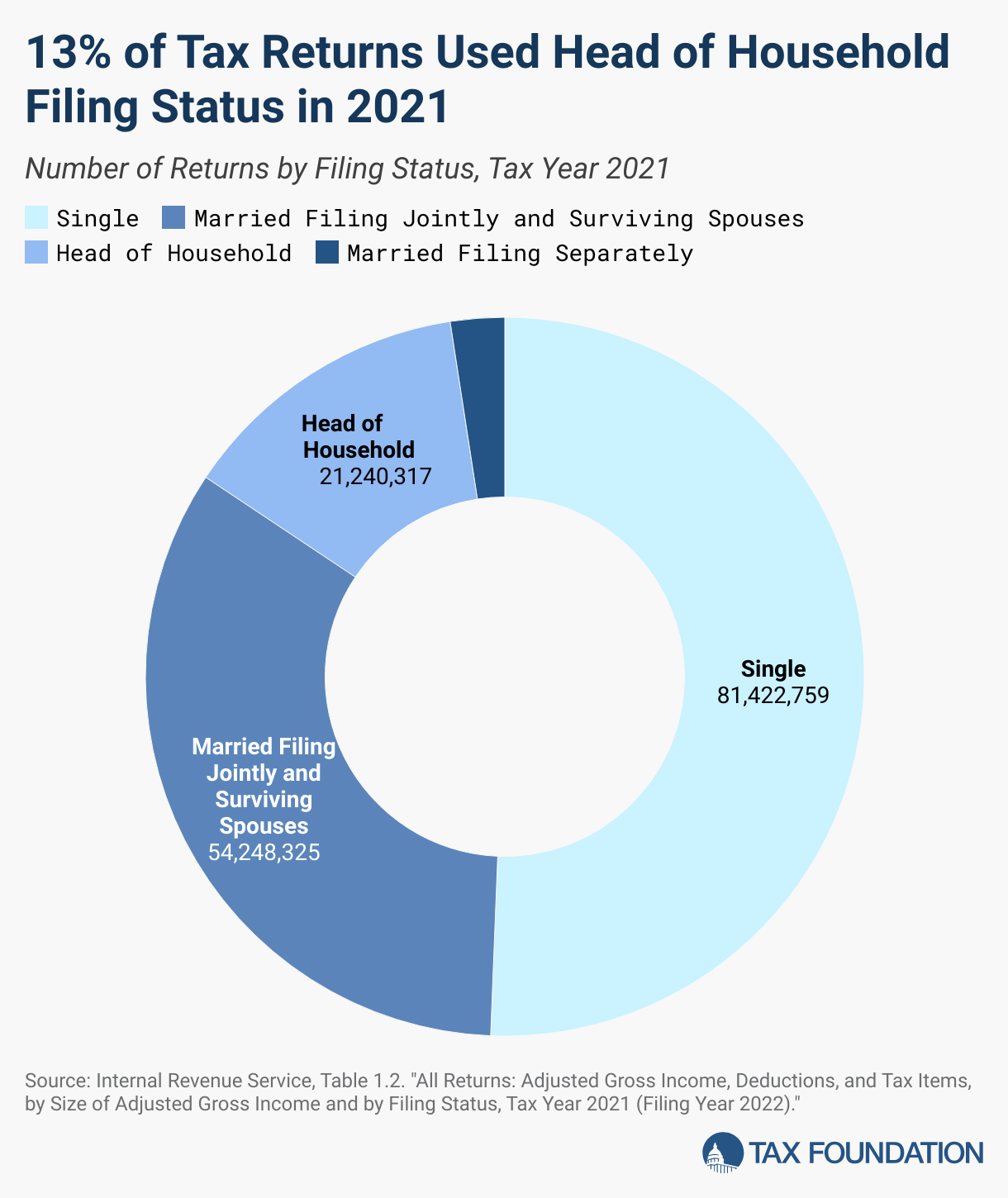

When filing their tax returns, US taxpayers choose among five filing statuses to determine the size of the standard deduction they qualify for and the thresholds at which different tax rates or phase-ins and phaseouts begin. Of the five filing statuses—single, married filing jointly, married filing separately, head of household, and qualifying surviving spouse—more than 84 percent of filers chose either single or married filing jointly/surviving spouse in tax year 2021. A much smaller group of filers, about 21.1 million, or 13 percent, filed as head of household in tax year 2021.

To file a head of household return, taxpayers must meet certain qualifications: be unmarried and pay more than half the cost of keeping up a home for themselves and a qualifying person living in the home with them for at least half the year. Meeting those criteria qualifies a head of household filer for certain tax breaks, including a larger standard deduction and wider tax bracketsA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat.

than single filers.

The head of household filing status is designed to help single parents who take on the primary responsibility of caring for a dependent. In doing so, however, it creates a marriage penaltyA marriage penalty is when a household’s overall tax bill increases due to a couple marrying and filing taxes jointly. A marriage penalty typically occurs when two individuals with similar incomes marry; this is true for both high- and low-income couples.

, as joint filers with children do not receive a commensurate tax benefit for having children. For example, in 2025, the 12 percent tax bracket begins at $11,925 for single filers but $17,000 for head of household filers, saving head of household filers $102 in taxes based on these filers having qualifying dependents. Table 1 illustrates how a head of household filer who gets married would lose the $102 tax benefit, resulting in a marriage penalty.

Table 1 shows a single filer making $25,000 with a $2,762 tax liability and a head of household filer with a $2,660 tax liability. When these two filers are unmarried, their combined tax liability adds up to $5,422. But if they were to marry, their combined tax liability would rise to $5,523, as the head of household filer loses the $102 in tax savings from the wider brackets.

Head of household status also fails to fully adjust for differences in household size because it is based on the marital status of the taxpayer, rather than on the number of children the taxpayer has.

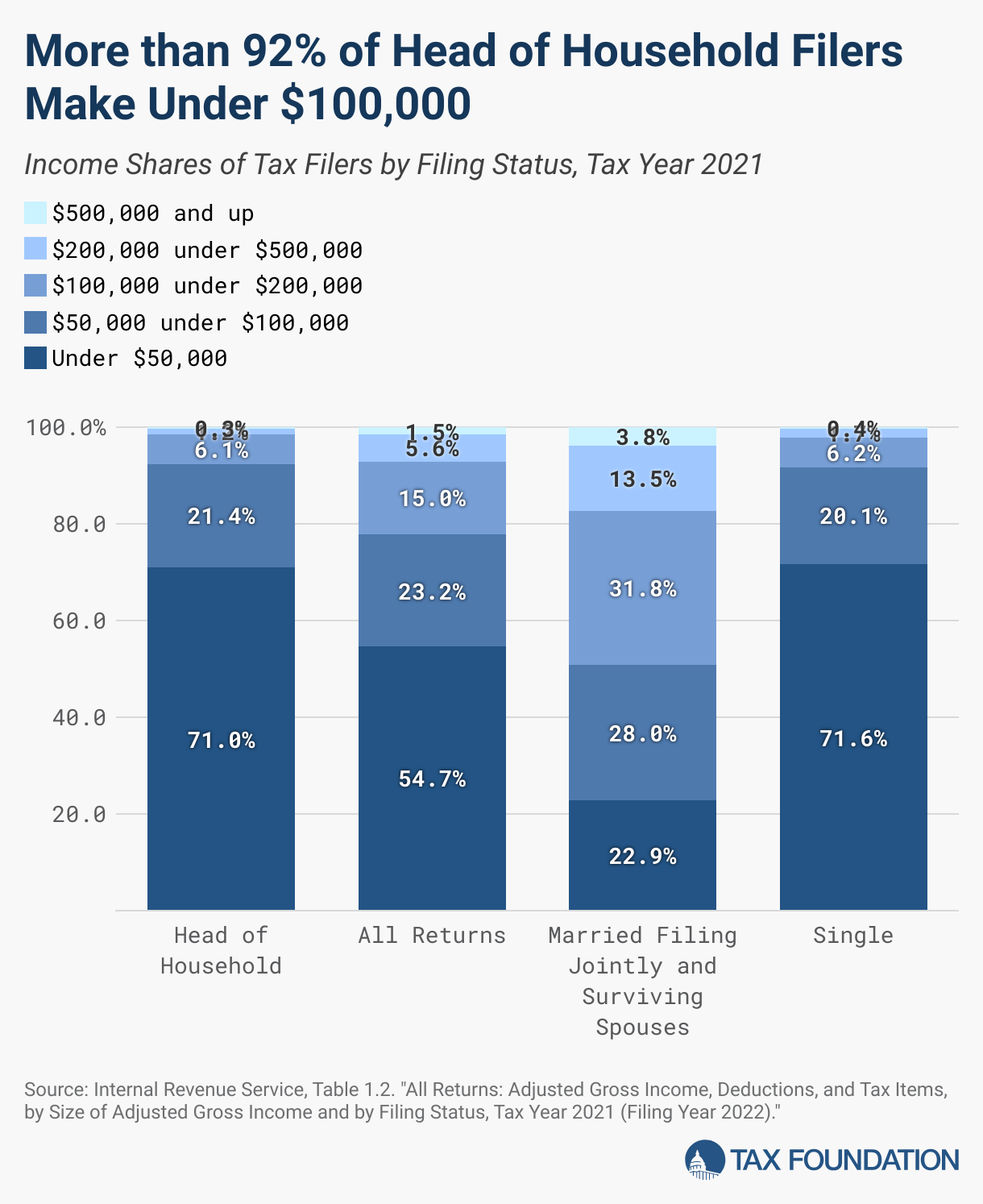

Head of household status is used primarily by lower-income filers. Filers making under $50,000 accounted for 71 percent of head of household returns in tax year 2021, and more than 92 percent of head of household returns reported under $100,000 of income, according to IRS data.

Repealing head of household filing status would move this group of filers to single filer thresholds and levels across the tax system. In 2025, for example, the standard deduction would be $15,000 instead of $22,500, a reduction of one-third. Tax brackets for lower-income filers would also kick in at lower levels of taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. For both individuals and corporations, taxable income differs from—and is less than—gross income.

based on single filer status: in 2025, the 12 percent bracket would start at $11,925 of taxable income instead of at $17,000 while the 22 percent bracket would start at $48,475 instead of at $64,850.

Thresholds for the next brackets are already equal to single filer thresholds, so higher-income taxpayers would not see a difference in their marginal tax rates. Similarly, the capital gains taxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. These taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment.

brackets would shift to single filer thresholds.

We estimate that on its own, repealing head of household filing status would increase tax revenue by $250 billion from 2025 through 2034. One complication, of course, is that the changes made by the 2017 tax law are scheduled to expire beginning in 2026, which explains the difference in the revenue score between 2025 ($27.1 billion), when the TCJA is still in effect, and 2026 ($20.0 billion), after it has expired.

In the context of first making the TCJA’s individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S.

changes permanent, which would reduce federal tax revenue by $3.4 trillion, repealing head of household status would raise $346 billion, offsetting about 10 percent of the cost of TCJA individual permanence.

Repealing head of household filing status would have a negative impact on economic output by subjecting taxpayers to higher marginal tax rates. We estimate head of household status repeal would produce a 0.1 percent smaller long-run economy, a 0.1 percent smaller capital stock, and 106,000 fewer full-time equivalent jobs. If repeal instead provided lower tax rates to this group of filers, it could have a positive impact on economic output.

Repealing head of household status on its own would reduce after-tax incomes, particularly for taxpayers in the 20th to 80th percentiles. Filers in the bottom and top 20 percent of earners would see smaller decreases in after-tax incomes from repealing head of household filing status. On average, filers would see a 0.2 percent decrease in after-tax incomes in 2025 and over the long-run.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Share this article